We have been speaking to a lot of clients over the last weeks about their investments due to the market volatility, but also those that are affected from an Income point of view. Here are the most Frequently Asked Questions and some brief answers to help you, if you have the same questions.

Please remember these answers are of a general nature and do not take into consideration your current circumstances. If you need specific advice, please contact one of our Advisers. We endeavour to keep these responses as accurate as possible, but given the constantly changing situation some of the items may be changed. We will endeavour to update as new information and questions come to light. Last updated 31/3/20

Q: Should I stop my super / investment contributions during the crisis?

A: Buying investments when the markets are down is much better value in the long run than buying when markets are high. Things are cheaper and the risk are lowers than they were before because a lot of the negative news is already factored into the prices. It may get worse before it gets better, but it is possible to buy investments 15-30% cheaper than they were a month or so ago.

IMPORTANT CAVEAT: The current COVID-19 situation is more than just a market drop, there is going to be widespread unemployment as well due to lockdowns. You need to make sure that you can afford to lock the money away in your super or investment and won’t need it to meet living expenses. If you don’t have good levels of emergency savings in place and your job security is low, then it may be prudent to keep the cash available until there is more certainty.

Q: Can I claim on my Income Protection if I have been laid off work?

Unfortunately, an Income Protection policy covers you if you are “unable to work due to illness or injury” not because work has stopped due to Coronavirus or other reasons. There are a couple of policies in the market that may have a redundancy clause in them which may pay you an amount of cover for up to 3 months.

Some polices have “Involuntary Unemployment” clauses that will either stop the Insurance premiums for 3 – 6 months so you can retain the cover without the cost (Beneficial if you do get ill and can’t return to work) or some help you cover mortgage payments in certain circumstances.

You can check the Product Disclosure Statement for your Policy and search for “Unemployment” or “Redundancy” to find out more.

Some also offer Premium Freeze, where you can stop premiums for up to 12 months, however you won’t be able to claim during this time. The benefit is you can unpause when you are ready and don’t have to reapply.

We have been speaking to many of the main Personal Insurers to see if they will adjust any of the clauses to help more people access the Unemployment benefits due to Covid-19. Most are currently offering ad hoc waivers but are currently deciding on blanket measures to be announced soon.

If all of the above options are exhausted and you do have to stop the premiums to “make ends meet”, we usually suggest the option of removing your payment details from the policy so that the policy becomes overdue and eventually lapses (60-90 days later) rather than cancel it outright. This way if you do need to claim in that period, you still have the ability to back pay the premiums and go on claim.

Q: Will my Insurer pay if I catch Covid-19?

Most fully underwritten Insurance policies do not have an exclusion for Pandemics or Infectious Diseases (however check your PDS). So if you have these policies, catch Covid-19 and can’t work or return to work for longer than your waiting period you will be able to make a claim.

However, many Superfund insurance policies or Direct Insurance policies have an exclusion for Infectious Diseases or pandemics that can be activated with 14 or 30 days notice.

If you take out a new policy currently, the Insurer may impose an exclusion for Covid-19 on the policy if you are high risk. Make sure you check the PDS exclusions before taking on any new cover and cancelling current cover.

Q: What is the new Jobkeeper payment and how do I apply?

A: On 30/3/2020 the Government announced a 6 month Wage Subsidy for employees of businesses whose revenue has dropped by more than 30%. If they qualify they can receive $1,500 per fortnight subsidy to cover some or all of your wages. You cannot apply for this, your employer does. We recommend that you contact them after the 2nd April (once they have time to process the new rules) to see if they will pursue this. New Zealand citizens on a 444 Visa will be entitled to the JobKeeper support payments.

If you are already on the Jobseeker payment list you can transition over easily so we recommend you still register your intent to claim on Jobseeker if your partners income is under the Income test.

Q: I’m lost my job or my income has dropped significantly, how do I apply for the Jobseeker payment?

A: Here is a great article that explains step by step how to access the payment whether you are new to Centrelink or already have a CRN. Be patient, the systems are overloaded currently.

We have also created an Action Plan for anyone who has lost their jobs or had a significant cut in income. Click here to download it.

Q: How much can we earn and still qualify for the Jobseeker payment?

A: If you are out of work and your partner earns less than $3,061 per fortnight (announced 30/3/20), you should qualify for the full Jobseeker payment.

From April 27th, if you’re a Casual, self employed or Sole trader and your income has dropped by 20% or more due to Covid-19 changes, you may qualify if you earn under $1,075 per fortnight.

If you qualify for $1pf of Jobseeker, you will also receive the new $550pf Stimulus payment.

Q: I have loans for my home or business, what should I do?

A: All banks are offering 3m plus mortgage deferments and some have a raft of other measures available to help clients such as interest rate cuts, fixed interest break fees waived etc.

Here is a good summary from our Lending team on what is available.

First step is contact your bank to ask for help and if you need more, get in touch with us and we will get one of the lending team to help whether you are an existing client or not.

Q: I’m already on Centrelink, do I have to do anything to get the $750 stimulus payments or additional $550 Jobseeker payment?

A: The short answer is No. These will be paid to you automatically. Centrelink has urged anyone in this situation to stop calling and logging on as it is adding unnecessary delays.

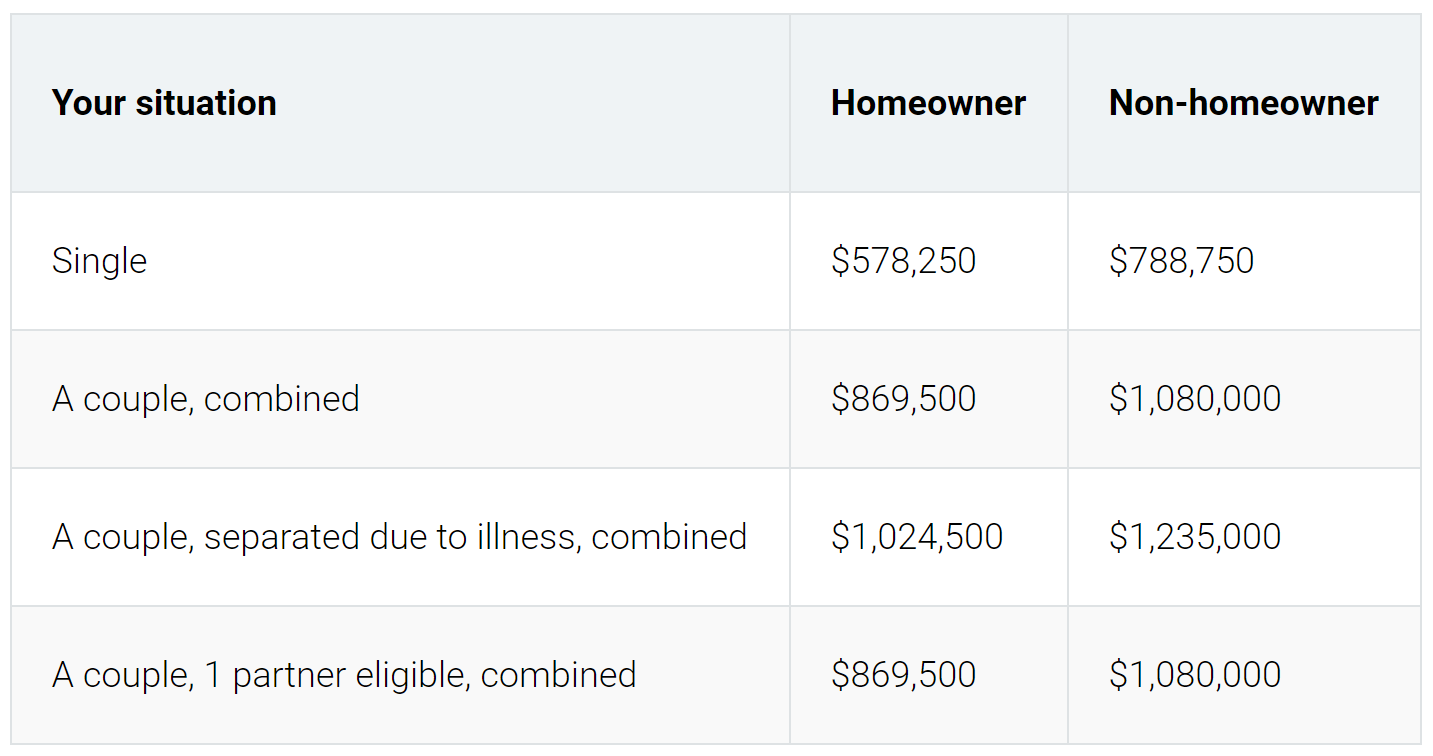

Q: Since my assets have dropped in value, when can I apply for a part pension?

If you are over Age Pension age and have not been able to claim a Pension due to your Assets being too high, with the current market correction you may find you are eligible to apply for a Part Pension. This may also entitle you to other Government Payments announced in the Stimulus.

Here is the link to see what is included in your asset test and what isn’t

Q: Should I be doing something with my investments / super or should I ride it out? Should I be selling my investments so they don’t go down to $0?

A: Nick Bruining said it so eloquently in his recent update we thought we would share his thoughts rather than write our own…

Last night’s performance of the US share market is why it is SO dangerous bailing out of fundamentally good quality investments in times of great turmoil. The US stock market surged 11.3 percent. I’m pretty sure it is the largest ever increase in a single day. Your trigger point “to get out” may have been Monday when our market dropped 8 percent. Feedback from the super funds tells me that call-centres overheated. (it might also have been people wanting to get their $10,000). Then, out of the blue came pronouncements that the the US Federal Reserve would NOT allow the system to fail. They have put their money where their mouth is and stumped up Trillions. It looks like the circus, otherwise known as the US Congress and senate, look like passing direct stimuli, much like our government – but $2 Trillion dollars worth. They’re also encouraged by further data that in some countries, the virus infection rate is now on the other side of the curve And starting to decline.

1) your super isn’t actually an investment Itself. imagine it’s a tax-efficient box that holds the ACTUAL investments.

2) depending on your fund, it will hold a mixture of actual investments in Cash, Fixed interest, buildings, infrastructure assets like toll-roads, pipe-lines and it will hold shares in real companies listed on the stock exchange.

3) the buildings, the toll-roads, the pipe-lines have gone nowhere. Did they crumble overnight ? No. Just like your house price, the values have dropped but the good quality asset is still there.

4) the shares are real companies that own real assets. Your super fund has big holdings of shares in BHP, Rio, Woolies, Wesfarmers, Apple, Samsung, BP and others. For your super fund to fall to nothing, all of these companies – ALL OF THEM – would have to disappear. That is not going to happen.

Absolutely the values have fallen. But as last night has shown us, things can change VERY VERY quickly and by the time you work that out, you may have easily missed out on a 20 percent gain, having locked in your losses by converting to cash at the bottom.

“Ride this thing out” is not a glib, throw away line. It’s the best advice you’ll hear.

It Is scary, values are swinging like I’ve seen before. 1987, 2001, 2008.

Remember the GFC. The “probable collapse of the world banking system” saw the Aussie share market plunge from about 7,000 to about 3,300. In the past few weeks, we’ve gone from a smidge over 7,000 down to 4,400. If you like, we’ve still got a 1,000 to go till we get to the 2008 numbers. That might happen, but look what happened then? Up it went. Fast and lots. To this day, I have people lamenting that they sold everything at the bottom by switching their super to cash. Needless to say, not clients of mine !

Every time a shock happens, we learn more on how to manage things. Even off the back of the GFC, the speed at which regulators and central banks have stepped in this time, has been mind-blowingly good. It seems to be working. I have no idea what happens next. It may well plunge more. Equally, it may have set it‘s low and now start to head up.

We’ll only know afterwards but ones thing’s for sure, some time in the future, we’ll be back through that 7,000 level again…